At the Open Travel Advisory meeting in Las Vegas this past week Henry Harteveldt from Forrester showed that Q1 numbers were down 1.6% in terms of transactions.

I have previously shown that the numbers for the OTA's are also off. Yet digging through Expedia's numbers the information basically points to a lowering of the transactions in air for the US domestic market but not the dollar numbers.

With Expedia's market share in the OLTA bookings at about 41% and stable - we can only think that there is some erosion and share shift amongst the other players. Expedia's share of traffic as measured in UVs seems to have declined in Q1 but there are discrepancies between the Comscore and Hitwise numbers. The former showing stability the latter showing a decline.

Thus we can conclude that Orbitz and Travelocity probably experienced a decline while Priceline grew - ditto Kayak.

With Orbitz isolated in that it cannot sell American Airlines product, we can see that the situation for Orbitz will not be pretty when they report their numbers in the next few days - May 5th to be precise. Click here to listen to the Webcast.

Things will be interesting for a while.

Cheers

29 April 2011

Mobile Trust and Privacy - Now A Major Motion Picture

Starring Steve Jobs and Larry Page as the evil villains. With Cameo roles by just about everybody.

This major disaster movie should rival epic disaster movies such as The Towering Inferno.

OK so enough of the fun - let's get down to the serious issues. As users and developers rush into mobile and the desktop starts to be less and less sexy to developers - the process of development has fallen into two camps. Lazy coders and evil coders.

One would be tempted to assume that no one does things for overtly evil reasons. But they do. In the case of mobile the number of pigs snouts in the trough is actually increased. Everyone wants to be like Apple - gouging themselves on as many possible revenue streams as possible. The poor longer tail players are left to pick over the consumer's carcass for some way to get some revenue. Trust the Cringe to give us a good perspective on this.

The convergence of these forces results in some pretty bad behaviour by the developers and anyone who wants to provide services. Fortunately on the web nothing gets hidden for long. God bless the transparency and those people who are just so darn curious for their 5 minutes of fame and at monitoring the big players.

So what of the general consumer. Fred Bloggs, Jean Marie, John Q Public etc etc. These guys our generalist consumer is very trusting. More so in the USA than in Europe. In other geographies - it is expected that monitoring is a standard form off behaviour for big government and big business. Good luck to them!

But this is not good enough. Despite the warnings from the Professor amongst a failure large chorus of players who have been trying to bring to the consumer these issues - we now have some major lapses and indeed solid evidence that there has been evil going on and these companies have been player fast and loose with our private information.

As I have opined many many times - there are two parts to messing with our privacy. First you have to actually monitor behaviour. Second you have to do something with that information. Most people have assumed that the monitoring is benign. Therefore the focus up till now has been on the misuse/abuse of the information collected. Indeed this is perhaps a defining characteristic that separates the European approach to the US approach towards privacy. The US approach says you can do about anything you like but dont mess with the stuff afterwards to take advantage. It also works on the 11th Commandment principal - "Thou Shalt Not Be Caught".

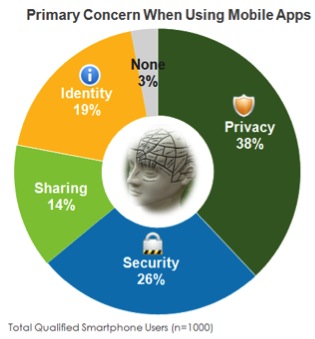

So lets's now look at some hard data. A good report by eTrust and Harris Interactive shows that actually contrary to the way the mobile players have been trying to hide this issue under the carpet the consumers have started to really appreciate the problems. And yes they are getting really concerned. From a study conducted in February 2011 - IE long before the relevations of the transgressions by Apple and Google in mobile - consumers had showed they were getting very nervous. about the top 3 issues of privacy, security and identity.

You can download the whole report at the link above.

You can download the whole report at the link above.Infoworld went even further to address the issue form the developers point of view. Click on this story "Why Users Dont Trust Mobile Apps".

Just in case developers think they can get away with it - I would not advise you to make that assumption. From the Harris/eTrust survey:

So now we are all just a little bit aware. Despite the Black Turle'd One coming off his sick bed to try and quell the storm , the cat is out of the bag.

And this time Steve McQueen is not going to be rescuing the bad dudes. And as in all good disaster movies - The bad guys will perish.

Cheers

Sabre's Kroeger Video: Airlines and Bloggers Say Travel Agents Are Not Innovative

I am not in favour of personal attacks on anyone. However, I feel somewhat obliged to defend the honour of the blogger community against perhaps some unfounded accusations.

I was sent me a link to a recent video message from Sabre's Chris Kroger to their travel agents. There is no disclaimer on here so I am assuming that the information is publicly available and freely distributed to the whole world through the wonders of the Internet.

In this message he is proclaiming Sabre's Innovation. More of the content of how he defines Sabre's prowess in innovation - later.

In the message he states:

"Recently there have been a few airlines and a few bloggers who have accused Sabre of being 30 year old technology and not innovating. And in some ways they are saying the same thing about you (the audience is Sabre Travel Agency Customers) a user of Sabre Solutions."

As a point of order if anyone is going to accuse Sabre of being old - let's go with a better start date of around 1960. (Source Wikipedia). When Sabre was started inside American Airlines and subsequently became part of AMR Corp. it was spun out as a separate company in 2000. If we are to accuse Sabre of being old - let's go with 50 year old technology.

His charge that some airlines and some bloggers have accused Sabre of being 30 year old technology does carry a lot of weight. There are many parts of the Sabre system that are indeed running robustly today and that are of that age. Robert Wiseman (Sabre Holdings CTO) since joining from rival Travelport in May of 2006 and his team have done a lot to modernize the Sabre infrastructure and keep it running. Robert is the man who overseas the "Hundreds of Millions of Dollars to ensure that our system architecture remains modern and robust... through modern protocol..." that Kroeger describes in his little talk. But we cannot deny that the platform is old technology and based on a 50 year old design. And that is not necessarily bad. It works. However is it appropriate for today's market? That depends on the position that you take with regard to what Sabre is today. In my view - it is old fashioned and it does need to be reformed to provide an open solution to the world.

I want to be clear that this is not to say that Sabre cannot do innovation - it clearly can. The question is more does it feel it needs to do significant amounts of innovation? EG Moving from a legacy architecture to one that meets the need of the customer of 2011 rather than the long extinct customer of 1960 is no trivial matter. Are they doing so? They claim to be - you are the judge.

Sabre is no longer willing nor able to provide a complete cradle to grave solution for every agency. Nor should it have to.

However has Sabre relied on innovation to maintain its dominant position in the marketplace or other means is a good question. In the view of US Airways - it is not Sabre's lack of innovation that has caused them to file suit against the Texas based company. It could be construed as a contributing factor however.

In his own words let's just let Kroeger tell us how he thinks that Sabre is an innovator.

"The Average Age of the hardware inside our environment is less than three years old". Yet he neglected to say how old the software was. It would be very interesting to hear that answer.

So here is my challenge to Chris Kroeger. Why not tell us what the age of the software modules are in the Sabre system. Come up with a verifiable metric so we can get an idea of how old the platform really is.

If Sabre's PEEPS provide this - I would be more than happy to publish this information. Perhaps then we can have an open and honest debate as to whether Sabre is truly modern and innovating in the same league as the other three companies he alluded to namely, Facebook, Google and Twitter.

Let me try to answer the question we started with. "Are Travel Agents innovative?" To me that is easy yes - they really are. This is the ONLY way to survive. Do they universally look to Sabre as the leading innovator in distribution? I think that would be an interesting question which in my view they do not necessarily feel so positive about.

Sabre Travel Information Network claims that it is "Powering Progress". In my view sadly its business practices are doing exactly the opposite. That has nothing to do with either their software or their hardware but more to do with their contracts and their lawyers.

And what do you think? agree with me or not? Let me know. In the mean time - let's see what can be done about powering real innovation in the market through providing next generation solutions for the consumer in an increasingly complex world.

Gotta love this business - the oldies love to dress themselves up on a cloak of innovation rhetoric.

Cheers

PS - If we are counting - I guess I am older than Sabre. And just remember what Sabre (an IBM expression from the 1950s) actually stood for.

26 April 2011

PSST - Wanna Know Why Expedia Settled With AA?

OK I did say that I thought this would come out in the end and that March would be the tell tale month for the online agencies.

Have a look the latest numbers from ARC.

The green line is the one....

The dragging down of the whole Intermediary market in the USA has been driven by the falling traffic from the OTAs. Now down more than 10% for 2 months in a row.

This shows you why Expedia realized that the removal of a key airline partner destroyed the consumer proposition of neutrality. I believe we will see these numbers moderate and the loss of share by the OTAs go a little higher next month but still negative in comparison to last year. Thus the kiss and make up session was bound to happen.

HOWEVER - there has been some permanent damage done. The overall share loss by the OTAs as a whole may be lost for ever to the direct channels.

I wonder how Orbitz are feeling right now.

Cheers

Have a look the latest numbers from ARC.

The green line is the one....

The dragging down of the whole Intermediary market in the USA has been driven by the falling traffic from the OTAs. Now down more than 10% for 2 months in a row.

This shows you why Expedia realized that the removal of a key airline partner destroyed the consumer proposition of neutrality. I believe we will see these numbers moderate and the loss of share by the OTAs go a little higher next month but still negative in comparison to last year. Thus the kiss and make up session was bound to happen.

HOWEVER - there has been some permanent damage done. The overall share loss by the OTAs as a whole may be lost for ever to the direct channels.

I wonder how Orbitz are feeling right now.

Cheers

25 April 2011

Telling The Truth

In today's ever transparent world, lying is clearly not a good thing. You WILL be found out.

However advertising is full of spin and innuendo as well as half truths and those little white lies.

One of the key values that Social Media is demonstrating the relationship between content and brand. What we used to call editorial content in days of Yore.

Check out this video from Scribe Media.

This is very important. And the end line advice to brands?

“tell the truth… and lots of it.”

Cheers

However advertising is full of spin and innuendo as well as half truths and those little white lies.

One of the key values that Social Media is demonstrating the relationship between content and brand. What we used to call editorial content in days of Yore.

Check out this video from Scribe Media.

This is very important. And the end line advice to brands?

“tell the truth… and lots of it.”

Cheers

Legal Opinion On Google ITA

When Google was trying to get approval for the ITA acquisition. I opined that there was little that the DoJ could invoke to prevent the merger.

Now with the dust having settled and Jeremy and the Gang have now been assimilated into the Googleplex we can see if I was right.

I scouted around looking for opinions on the approval.

Here is what I found that you might find interesting

I urge you to read this piece from the Washington Legal Foundation.

Enjoy it

Cheers

Now with the dust having settled and Jeremy and the Gang have now been assimilated into the Googleplex we can see if I was right.

I scouted around looking for opinions on the approval.

Here is what I found that you might find interesting

I urge you to read this piece from the Washington Legal Foundation.

Enjoy it

Cheers

Is It All Really JUST About The Money? Airlines & GDSs To Duke It Out In Court

Sabre and Travelport - both private companies - have become the target of 2 lawsuits alleging Anti Trust behavior by AMR's American Airlines unit and US Airways. American Airlines is suing Travelport and its affiliate public company Orbitz (OWW). US Airways is suing Sabre. Both suits are similar in nature. At stake is the very nature of airline distribution in not just the USA but around the world. This analysis will hopefully provide the context of the battle. Sabre is controlled by 2 players - TPG and Silverlake Partners. Travelport is largely controlled by Blackstone.

It seems to have been a really busy time in airline distribution lately. We have had many things going on – so perhaps we should consider what is driving some of the changes going on. For many who are in the business – this battle has been a long time coming. However for the rest of the world and many others – this has caused a strong degree of head scratching. Consider this a primer on the core issue of control.

Let's just look at some of the major issues that have surfaces since October. This was the month when AA's battle with Orbitz burst into the open. Soon to be joined by Travelport, Expedia, and Sabre. Just looking at the last few weeks - I don't think we have seen such activity in a long time. Here is a list of some of the news stories over the past few weeks that have seemed to be disconnected. Here is a partial list:

• Expedia settled its battle with AA and committed to a Direct Connect – in doing so Expedia abandoned the GDS only model and agreed to go the direct connect route as well as signing its first LCC for Direct Connect – Air Asia in a far reaching Joint Venture.

• Delta Airlines signs with Farelogix to create alternative distribution services for the nation’s second largest carrier making a clean sweep of all the major North American carriers are now signed up to participate with the Farelogix platform. AC, UA, CO, AA, DL, US. Delta also makes the 13th Airline to have publicly committed to the system.

• The FAA Re-authorization bill passed without the GDS provisions that were defeated 3 times during the passage of the bill.

• The DoT issued new passenger regulations but in issuing this new "Passenger Bill of Rights" it declined to force (for the short term at least) provisions which would have made the airlines display ancillary services via the GDS.

• AA filed suit against Travelport and its affiliate company Orbitz Worldwide (owned 48% by Travelport) alleging anti trust behavior.

• US Airways filed suit against Sabre also alleging anti trust behavior.

• The DoJ after a lengthy evaluation approved the Google/ITA deal – the deal has now closed.

Are these unrelated? I don’t think so. But let me just focus on the 2 lawsuits.

For a minute let's just consider what is driving their thought processes. I am taking this from the perspective of the parties who filed the suits. We have not yet seen the defense other than both parties (Sabre and Travelport) has said they will vigorously defend their position. I have opined before that in my view Travelport’s statements lack some substance and so far have contained some factual inaccuracies but since they have not filed a formal brief – this can be construed as PR spin. . Don’t forget GDSs and Airlines can hire some pretty serious legal firepower. This battle is not new. Don’t think for a minute that the Airlines have not just woken up yesterday and said - "we're bored, let's go after the GDSs". This battle was clearly a very long time coming.

Both lawsuits (AA vs Travelport/OWW and US vs Sabre) are very explicit in what they want and the respective positions. While they appear to be similar - each airline comes from a very different space. The AA lawsuit is somewhat of a pre-position. The US suit is backward facing for the contract it already signed.

The AA lawsuit actually names Sabre several times in its suit against Travelport. AA has made its sentiments known that it feels the GDS model needs to change. Possibly after 9/11 and perhaps we can trace the lineage of the battle to the very moment that Sabre was spun out and AMR (AA's parent) put the resulting cash in its pocket. US Airways however is not quite in the same position. They are the smallest of the big airlines (Now comprising just 5 in the USA). They never owned a GDS. This makes them the least able to apply leverage in the ongoing battles. They also have effectively put themselves up for sale by delivering a message that consolidation is not yet over and that US Airways is ready to be merged into another airline - AA according to analysts - perhaps being the favorite. One could even opine that US is trying to ingratiate itself with AA. I make this point because I believe US Airways thus is not arguing from any position of strength. Ultimately in terms of scale we have to remember that the market share of each of the major American GDSs exceeds that of any airline in the USA market.

The driving forces for the lawsuits are that the airlines believe they asked nicely (well as nicely as an airline can) that the GDS behave differently. IE that the GDSs change their model. The GDSs refused both publicly and privately to budge. Indeed they went on to consider any change should be viewed as a nasty attack on their core business model, for which a vigorous defense needed to be mounted. Were the airlines napping on the job? Perhaps yes they were for a while. They thought they had a deal with the GDSs.

in 2006 the airlines and the GDSs entered into a form of social contract. The background at that time was that the GDSs were scared that the Airlines would provide content on their own websites that could not be seen on the GDSs. Thus moving both the trade as well as the consumer to more favourable content on the airlines own sites. The genesis of the Full Content Agreements was that the Airlines would give the GDSs full content in exchange for reduced fees. (I want to avoid using the term discounts which is how the GDSs saw this). This social contract worked pretty well because essentially all the major legacy carriers signed up for it.

In airline distribution - the traditional basis of the distribution landscape is one for all and all for one. Or as I prefer to characterize it as "one size fits everything." However the GDSs lawyers might have been smarter than the airlines' lawyers. Why? Because the GDSs managed to put in a number of provisions that created a far stricter contractual environment. So the issue of full content tied with a number of other provisions gave the GDSs a distinct edge. At the same time the GDSs started down a path of increased tighter contract provisions with their user community; the travel agents - the subscribers. In doing so they created a Gordian Knot. The airlines were trapped. The subscribers were trapped. The analogy - admittedly somewhat extreme - but humour me here I think you will find the comparison is not that odorous - it could be likened to a drug cartel (aka the GDSs) were able to control distribution.

But let’s not shed too many tears for the airlines. In the early part of the millennium the airlines ceased to provide compensation in the form of standardized sales commissions to the agencies. Thus the agency players and the airlines ceased to have a compensated relationship. They still however retained a contracted relationship either directly or via ARC. The corporate customers of the agencies allowed the water to flow downhill by paying the increased freight of an access fee for use of the agencies' services. Thus these agencies - TMCs - were able to transfer from a supplier paid fee model to a consumer paid fee model - a transition that went remarkably well. Even the leisure agents tried this for a while but this fell apart when Priceline refused to join the fee based model. In recent years the other OTAs - largest players such as Expedia and its fellows abandoned the fee model for leisure bookings. Sadly the independent small agents were not so lucky and this effort drove many of them out of business. From a peak in the mid 1990s to today the number of agency locations has collapsed from 55,000 to now below 20,00 outlets.

Thus there is dissonance in that the travel agents are in many cases not directly compensated for selling airlines product. This somewhat advantaged position works for the airlines because they regard their product as being valuable and that the consumer and their channels should pay to access the product. This conveniently forgets that the agents actually do add value in aggregating content for the creation of neutral offers to their consumers a core value proposition for the consumer.

The GDSs too started playing a number of games. Firstly they had created an artificial MSRP pricing structure and backed it up with the charade of saying they were providing large discounts to the airlines. How much of a charade? Even after allowing for the cut rate prices -Amadeus's margin in 2010 as provided by their annual reports show a margin of 48% on its GDS business alone. The other publicly available information for Travelport shows that its margins declined from a peak of 33% in mid 2009 to the current level of 28%. (Does Amadeus know something that Travelport doesn’t?) We can safely assume that Sabre is in the same ballpark. The average segment fee (net revenue) for each company was as follows:

Travelport – rose from $3.47 in Q1 2007 to $5.83 in Q4 2010.

For Amadeus we only have data from 2009 which shows the revenue per segment rose from (Q1 2009) $3.28 to just under $5. ($4.97 in Q4 2010) when converted from Euros to Dollars.

So despite the social contract between the GDSs and the airlines the actual cost to the airlines rose significantly during this time. NOTE I am using publicly available information and you can find this out for yourself on the websites of Travelport and Amadeus.

Indeed one could argue that the social contract was flawed to begin with but the GDSs (now fully controlled by the money guys in the form of Private Equity/Venture Capitalists) had obligations to increase their margins. How did they do that? They cut costs by slashing payrolls, cutting pure R&D and by changing their agreements.

In the case of Travelport there were significant synergies gained by the merging of the Worldspan and the Galileo businesses. However Travelport was upfront and said it would not bite the big one and merge its (now 3) GDSs into a single code base. In my analysis all the GDSs gained incremental net revenue through two techniques. Through unbundling their core segment fees, long before the airlines became effective at unbundling – the GDSs were doing this and made good money from it. But they also changed the contracts to further tie the airlines. At the other end they were able to generally reduce the cost of the subscriber delivery through cutting back on services. But the one area that they could not cut was in the segment incentive fees (aka as US Airways describes them “Kickbacks”). The competition for smaller pie – i.e. the reduced agent community – meant that the GDSs had to pay ever increasing incentives to the agencies to ensure a reliable user base. What happens is simply the GDSs take a portion of the fee that the airlines pay and kick back this portion to the travel agents.

To examine this - have a look at Travelport's 2007 and 2010 end of year financials.

2007

Cost of revenue.....................................$1,167

Selling, general and administrative......$1,286

Separation and restructuring charges.......$90

2010

Cost of revenue.....................................$1,164

Selling, general and administrative...........$547

Restructuring charges..............................$19

I think you get my point. During this time Travelport's segment count fell from 416.2 Million to 349.4 Million segments (all 2007 vs all 2010).

Rumours abound of the amounts paid not just to get agents to switch but also just to stay in place. These payments are so large in more than one market the asking price for a GDS segment incentive is $4.00. To cover this cost the GDSs must be indeed cross subsidizing the bigger agents (i.e. those with market power) from two places firstly the weaker and smaller agents who tend to be brick and mortar; secondly from those markets where they don’t have to provide incentives due to their market power – which today are very few.

In addition to the core issues above – the airlines feel that the GDSs have not kept up the investment in two key areas. Functionality to support the sale of ancillary and unbundled products (seats, bags credit card charges etc). The other charge is that the GDSs have actually inhibited the ability of the airlines to sell personalized services via the intermediary channels. For whatever reason - the GDSs do not provide these services today except in very few cases.

The core of the arguments that the airlines feel harmed is not just based on cost. But ultimately it is based on the argument of who controls distribution. So these lawsuits are about breaking the Gordian Knot.

Want to read some more?… actually you could have largely done a cut and paste of the law suits by going to a not quite so obscure website and downloading the Airlines comments on the US DoT NPRM concerning the Passengers Protection. Last week the US DoT turned this into law. Curiously only after two events. Event 1 - the Dept of Justice had approved the Google Acquisition of ITA Software. Event 2 – the FAA bill was approved by the US Congress. Coincidence?

The final rule making is here: DOT-OST-2010-0140

For AA’s comments on this rule making go here:

For US’s comments go here:

So now you know – where you sit in the debate should at the very least be powered by the information to hand.

I recommend that you go through the other submissions on the dockets. There is a lot of material in there. Then sit back and think – are these events connected? Yes. Is my answer. However the airlines feel emboldened by the changes coming. What we are seeing is nothing short of a fundamental shift in Airline distribution.

Catch the wave. Open Distribution is with us.

Cheers

24 April 2011

Do You REALLY Need To Change The Site?

In the web world - there is often an argument of change for change sake

Hey because the web changes so quickly you need your website to change too. The result is that you have big projects every year to change the site. People love to talk about "The New Website". Frequently that creates a groan from the user.

Just as he gets used to the new site and its changed navigation - along comes another one.

Making the argument for change is not hard. But do you ever ask yourself whether the change was really necessary. Would perhaps an incremental set of improvements have been better? Is this a wise use of the money?

Some sites cry out for re-design because they just get junked up or because they have new technology. Case in point the new Ryanair website.

A fun thing to do is to go to the WayBack machine. Have a look at some of the sites - like Expedia after a redesign. You will see how they tend to start clean after each redesign.

I heard a recent statistic that is really relevant to the Travel Sector. (This was quoted by Expedia in a recent webinar) the source was the IAB. The number of clicks before abandonment was 7 down from 13 a few years ago. This tells us that the customers are getting frustrated with sites. TOO much eye candy purporting to be "merchandising".

So now is the time to think - do I really need to change. If I am going to merchandise products and services or am I simply putting things in the path of the consumer that are unnecessary and will in turn piss them off.

I am still somewhat amazed that the Look to Book ration in Travel is so abysmal. It reeks of a lack of trust and clearly the site User Experience is driving a number of users away.

This week in my alter ego state I shall be moderating a panel on Airline Merchandising. I urge you to consider these issues. Finally here is a little piece this week from Gerry McGovern that takes these issues a little further.

Food for thought and ammunition to enable people to think more carefully.

Cheers

Hey because the web changes so quickly you need your website to change too. The result is that you have big projects every year to change the site. People love to talk about "The New Website". Frequently that creates a groan from the user.

Just as he gets used to the new site and its changed navigation - along comes another one.

Making the argument for change is not hard. But do you ever ask yourself whether the change was really necessary. Would perhaps an incremental set of improvements have been better? Is this a wise use of the money?

Some sites cry out for re-design because they just get junked up or because they have new technology. Case in point the new Ryanair website.

A fun thing to do is to go to the WayBack machine. Have a look at some of the sites - like Expedia after a redesign. You will see how they tend to start clean after each redesign.

I heard a recent statistic that is really relevant to the Travel Sector. (This was quoted by Expedia in a recent webinar) the source was the IAB. The number of clicks before abandonment was 7 down from 13 a few years ago. This tells us that the customers are getting frustrated with sites. TOO much eye candy purporting to be "merchandising".

So now is the time to think - do I really need to change. If I am going to merchandise products and services or am I simply putting things in the path of the consumer that are unnecessary and will in turn piss them off.

I am still somewhat amazed that the Look to Book ration in Travel is so abysmal. It reeks of a lack of trust and clearly the site User Experience is driving a number of users away.

This week in my alter ego state I shall be moderating a panel on Airline Merchandising. I urge you to consider these issues. Finally here is a little piece this week from Gerry McGovern that takes these issues a little further.

Food for thought and ammunition to enable people to think more carefully.

Cheers

Subscribe to:

Posts (Atom)